Building Wealth in 2026: Your Comprehensive Financial Playbook

Imagine starting 2026 debt-free, with a growing nest egg and the confidence to navigate economic uncertainties. That’s the vision laid out in a compelling YouTube video on financial strategies for the year ahead. Drawing from expert insights on budgeting, debt management, investing, and emerging trends like AI and inflation, this playbook isn’t just about crunching numbers—it’s about overcoming behavioral hurdles and taking actionable steps toward lasting security. In this blog post, we’ll break it down, embellished with the latest 2026 data, real-world examples, and practical tips to make it relevant today.

As of January 2026, with U.S. inflation holding steady at around 2.7% (based on December 2025 figures from the Bureau of Labor Statistics), and high-yield savings rates climbing up to 5.00% APY from providers like Varo Money, the opportunities for smart money moves are ripe. Let’s dive in.

Your Financial Foundation Deep Dive Video

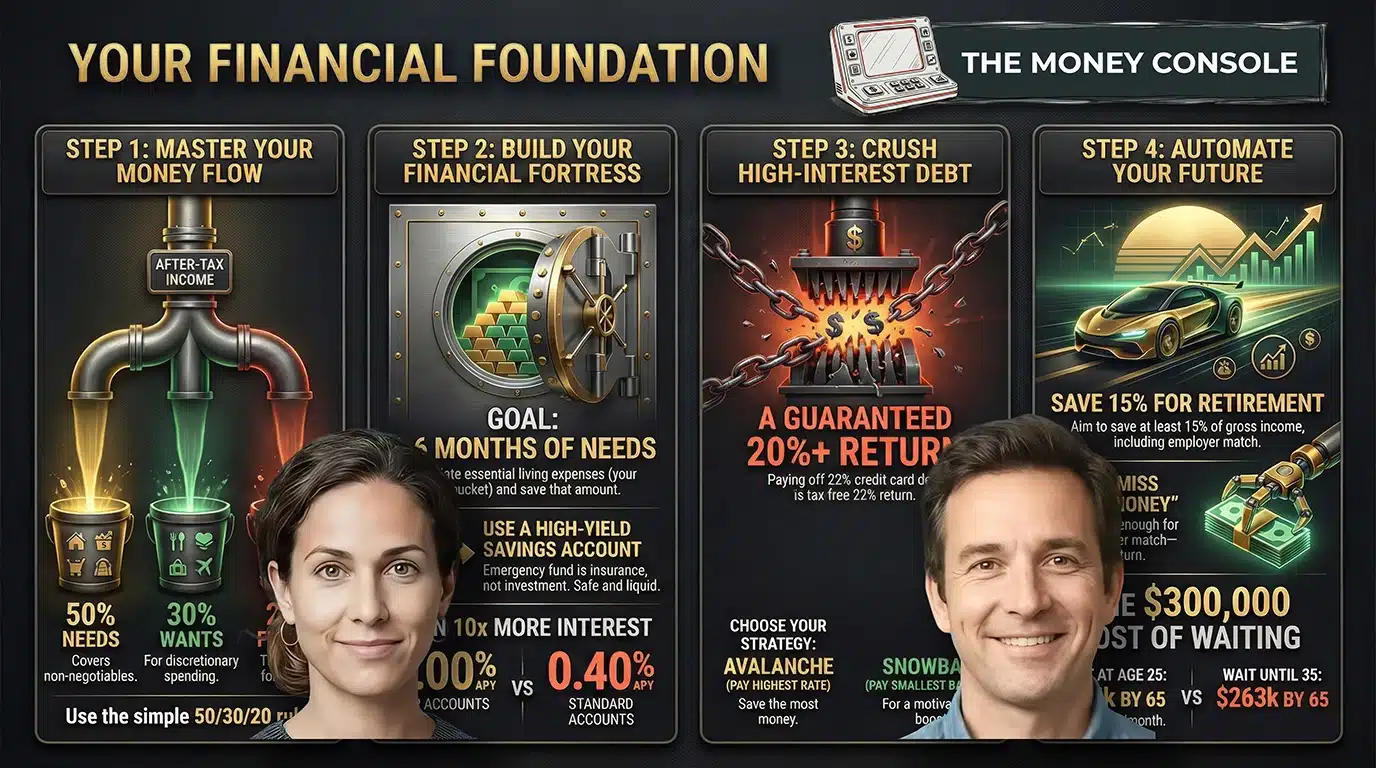

Mastering Your Cash Flow: The 50-30-20 Rule

Traditional budgeting can feel like a chore, tracking every latte and receipt until burnout sets in. Instead, embrace the 50-30-20 rule—a simple framework popularized by financial experts like Elizabeth Warren. This allocates your after-tax income into three buckets:

- 50% for Needs: Essentials like rent, groceries, utilities, insurance, and minimum debt payments. If you’re in a high-cost area like Orlando, Florida (where average rent hovers around $1,800 for a one-bedroom), this cap forces lifestyle adjustments to avoid “house poor” scenarios.

- 30% for Wants: Discretionary spending on dining out, entertainment, hobbies, or travel. This bucket keeps life enjoyable but acts as a buffer—if your wants creep up, trim here first to boost savings.

- 20% for Savings and Debt Repayment: The wealth-building engine, covering emergency funds, retirement contributions, and extra debt payoffs.

This rule works for beginners and seasoned pros alike. For instance, if your take-home pay is $5,000 monthly, that’s $2,500 for needs, $1,500 for wants, and $1,000 for future-proofing. Recent surveys show that sticking to this can help Americans, where the median household income is about $74,000, build resilience against economic dips.

To implement, use apps like Mint or YNAB (You Need A Budget) for automated tracking. Remember, the key is consistency—behavioral finance research from Nobel laureate Richard Thaler highlights how small, habitual changes override emotional spending impulses.

Building Your Financial Lifeline: The Emergency Fund

No financial plan survives without a safety net. Aim for 3-6 months of living expenses (focusing on your 50% needs bucket), or up to 9 months if you’re self-employed or in a volatile industry like tech. For a family with $4,000 monthly essentials, that’s $12,000-$24,000.

Real-life shocks abound: Data from 2025 shows 37% of U.S. adults tapped emergency savings for expenses averaging $1,000-$2,500, often for repairs or medical bills. Without this buffer, you’re forced into high-interest debt, undoing progress.

Park it in a high-yield savings account (HYSA) for safety and growth. In January 2026, top rates include 5.00% APY from Varo (on balances up to $5,000 with qualifications) and 4.35% from Newtek Bank. These outpace traditional savings (averaging 0.61%) and combat inflation’s 2.7% bite. Interest is taxable as ordinary income, so factor in a 1099-INT form, but it’s worth it—$10,000 at 4.5% earns $450 annually versus $61 in a standard account.

Start small: Automate $50 weekly transfers. Once full, redirect that 20% to debt or investments.

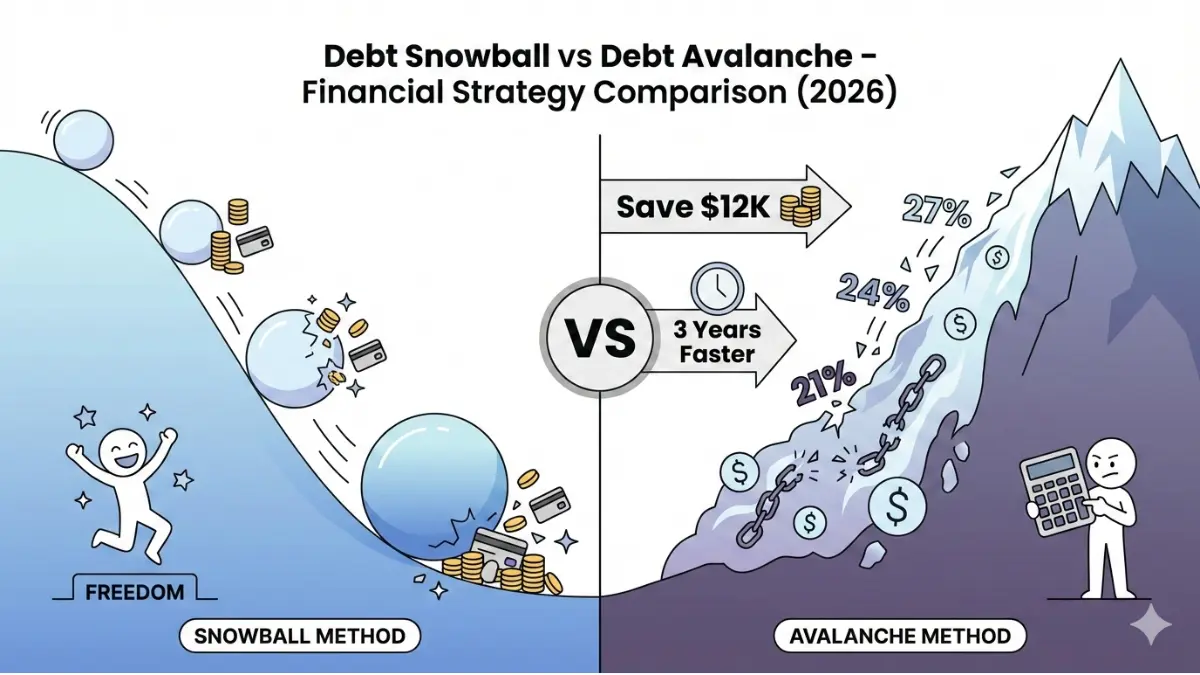

Crushing Debt: Strategies for Freedom

High-interest debt, like credit cards averaging 22% APR, erodes wealth faster than most investments grow. Paying it off equates to a guaranteed 22% return—unbeatable.

Prioritize unsecured debts first. Two proven methods:

| Method | How It Works | Pros | Cons | Best For |

|---|---|---|---|---|

| Debt Avalanche | Pay minimums on all debts; extra toward highest-interest first. | Saves most on interest (e.g., $10K at 22% vs. 15% saves hundreds). | Slower visible progress. | Math-focused individuals. |

| Debt Snowball | Pay minimums; extra toward smallest balance first, rolling payments. | Quick wins build momentum (e.g., clear a $500 card fast). | Higher total interest paid. | Those needing motivation. |

Snowball vs Avalanche Method

Consider consolidation via a personal loan at 10-15% if it simplifies payments—but only if you curb spending. Tools like Undebt.it simulate scenarios.

Navigating Buy Now, Pay Later (BNPL) in 2026

BNPL exploded, with global market value hitting $560 billion in 2025 and U.S. users reaching 90 million. It spreads costs interest-free but now impacts credit: FICO’s 2025 models (10 BNPL and 10T BNPL) factor in usage history, volume, and repayments.

Pros: Boosts spending by 72% per transaction. Cons: Multiple plans signal risk, potentially dinging scores. Average monthly BNPL spend rose 21% to $244 in mid-2025. Tip: Use autopay, limit to one at a time, and treat as debt.

Maintain credit health: 35% of your score is payment history (on-time always), 30% utilization (under 10% ideal). Check via AnnualCreditReport.com.

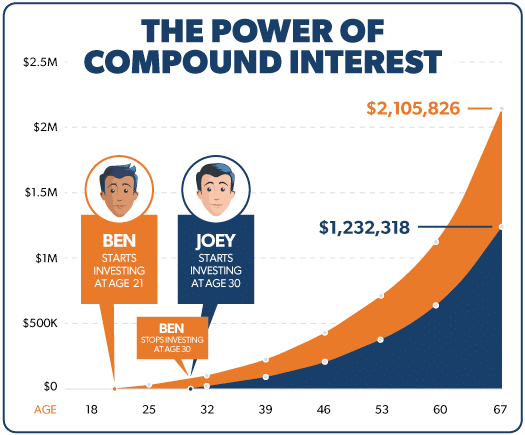

Harnessing Compounding: Invest for the Long Haul

Time is your ally. Saving $200 monthly at 7% from age 25 yields ~$575,000 by 65; starting at 35 drops it to $263,000—a $312,000 time cost.

Target 15% of gross income for retirement, including employer matches (free money—e.g., 50% on 6% contribution is instant 50% return). Secure the match first, then IRAs.

Roth vs. Traditional:

- Roth: After-tax contributions; tax-free growth/withdrawals. Ideal for young earners expecting higher future brackets. 2026 limit: $7,000 ($8,000 if 50+), phase-outs for high incomes.

- Traditional: Pre-tax deductions; taxed on withdrawal. Suits peak earners anticipating lower retirement taxes.

For beginners: Low-cost index ETFs (e.g., S&P 500 trackers like VOO) for 10% historical returns with diversification. Use dollar-cost averaging (DCA): Invest fixed amounts regularly to average costs and reduce timing risks.

The Power of Compound Interest

Gen Z beware: Social media hype leads to overconfidence; stick to education over influencers.

The New Frontier: AI, Inflation, and Advanced Tactics

AI transforms finance: 85% of firms use it for fraud detection and personalization. Apps like Acorns auto-save or optimize budgets, but watch for biases in lending algorithms.

Inflation persists at ~2.7%, driven by labor shortages and housing. Hedge with assets like REITs or commodities that rise with prices.

Tax optimization: Harvest losses to offset gains (up to $3,000 against income; carry forward extras). Avoid wash sales (61-day rule).

ESG investing grows, but greenwashing plagues it—regulators like the SEC demand proof beyond vague claims.

Your Path Forward

This playbook emphasizes discipline over drama. Start with 50-30-20, fund emergencies, crush debt, invest wisely, and stay vigilant on trends. Tools like AceMoney (mentioned in the video) simplify tracking.

Financial freedom is a marathon—question biases, seek diverse views, and act consistently. Subscribe for more insights, and remember: In 2026’s dynamic economy, your informed choices build unbreakable wealth. What’s your first step? Share in the comments!

Leave A Comment